At Fifth Ring we fully understand the energy industry. We comprehend the cyclical nature of boom and bust. We’ve helped our clients communicate out of downturns and maximised their visibility during upturns. But we’ve never known a time as crazy as this. And neither has the industry.

Never a dull moment? You bet. What optimism we had in January! There the industry was, with an oil price comfortably in the $60-$70 range, looking forward to a year of relative stability and comfortable revenue growth. Everything was running so smoothly.

Then along came COVID-19 and the world effectively stopped travelling. And just as the virus was starting to take hold in the Western Hemisphere, the OPEC+ group of producers, which had been doing a good job of managing global oil output and therefore prices, self-imploded because of a row between Saudi Arabia and Russia over quotas.

The oil price is creeping back up as the world starts to move once more, but we’re very far from being out of the woods. The Paris-based International Energy Agency (IEA) believes oil demand this year will show the largest fall in history of 8.1 million barrels per day. While the IEA is forecasting a 5.7 million barrels per day recovery in 2021 to 97.4 million barrels per day, that will still be some 2.4 million barrels per day short of 2019’s levels.

While we may see flash volatility as the world readjusts to post COVID-19 life, plus economic and geopolitical events, oil is unlikely to extend beyond $45 per barrel for sustained periods this year. Further out, companies such as BP have forecasted Brent crude will average $55 a barrel between 2021 and 2050. BloombergNEF estimates gasoline demand will peak in 2030. This ties in with pre-COVID-19 predictions from BP and others that oil’s share of global energy would grow to 2030 and then plateau.

In this new normal, there are three things leaders in the energy industry should consider.

We are in a demand-led market

For almost the whole of the 20th Century, we worried about running out of oil as vehicle sales grew and industrial requirements increased. But the US shale revolution at the beginning of this century ended that supply worry. Now the focus is on demand, and in the long term that demand is forecasted to decline. As one observer stated: “The price is telling us: ‘I’ve got plenty; don’t get me any more’.” Admittedly, shale is going through a challenging time due to the nuances of its investment models, and several companies are hurting – the most high-profile example being Chesapeake Energy recently filing for Chapter 11 bankruptcy. But, as soon as production becomes economically viable, whatever’s left of the shale sector will come back strongly.

The main thing that’s keeping oil prices afloat artificially right now is the record high production cut of 9.7 million barrels a day agreed by the OPEC+ members at an emergency meeting in April. These cuts are expected to ease incrementally as demand returns, but it’s a delicate balance with potentially disastrous pitfalls. Any further fall out within this group, or between OPEC+ and other producers such as the US, could trigger another supply flood and a price crash once again.

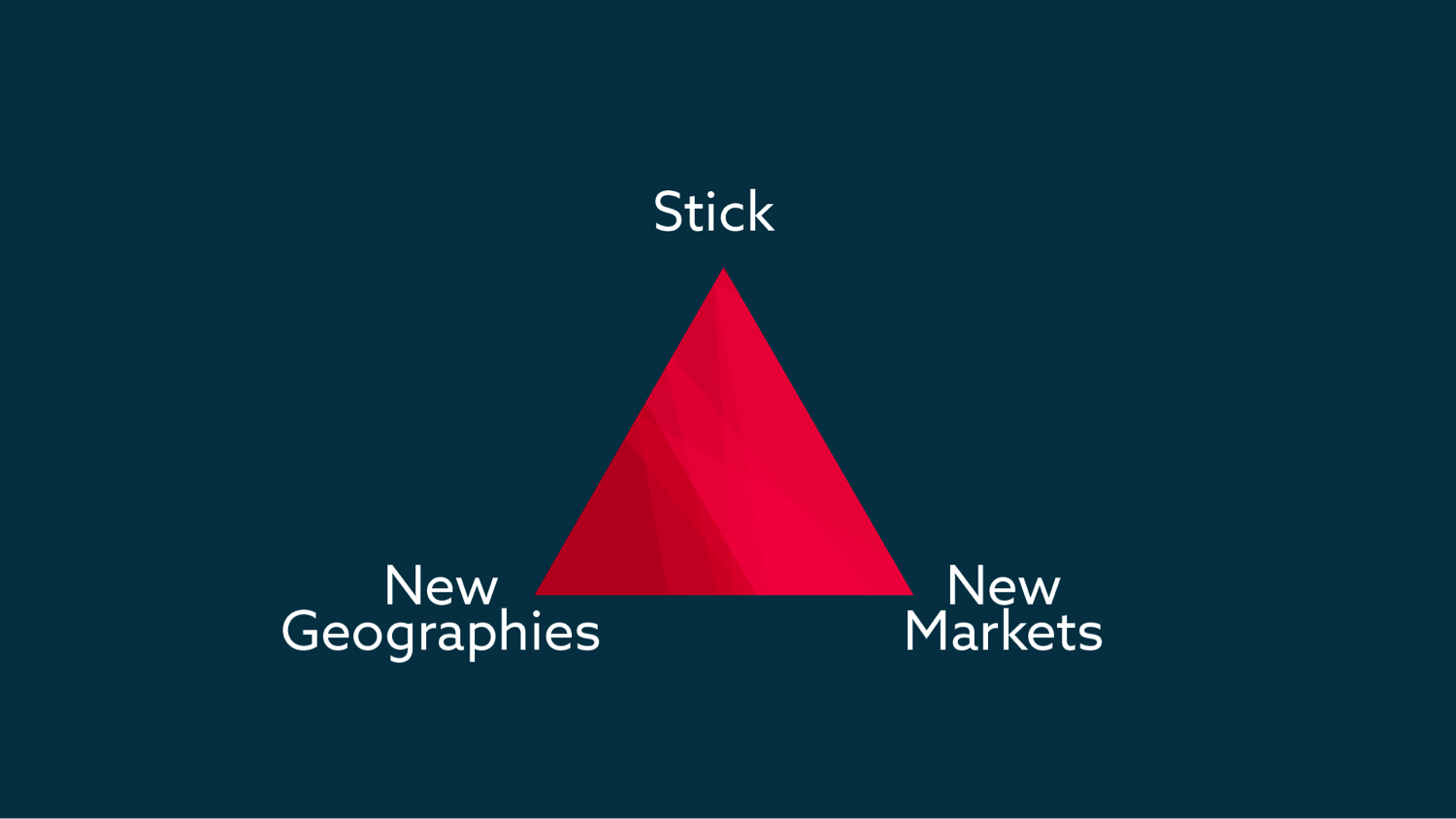

The energy trilemma

So, if the energy industry is increasingly more challenging what should companies do? There are three options. Firstly, they can continue to operate in their existing markets and become number one at what they do through differentiators such as new technology adoption, innovative business models or greater cost efficiencies. Secondly, they can expand their existing offering into new geographies (for example UK subsea companies supporting the Brazilian industry). Thirdly, they can explore new business verticals such as infrastructure provision for the offshore wind sector.

Energy is changing

Much has been made recently of the energy transition. Equinor, BP, Shell, Total and Eni announced their commitment to net-zero emissions strategies at the beginning of this year. More recently, the leaders of Shell and BP have questioned what the demand for oil will look like post-COVID-19 and BP has divested its petrochemical business.

While there is still plenty to play for in the oil and gas industry, and there will be for years to come, for the longevity of their businesses, CEOs should be thinking now about what these trends will mean for their operations.

Communication is key

The time is right for oil and gas companies to review their business proposition and their markets. An essential output of that will be effective communication with their stakeholders.

If their focus is on improving margins in existing markets they have to stand out from the crowd. If they are diverging into new geographies or verticals, they have to explain their story fully, externally and internally so that everyone gets and buys in to what they are doing.

We can help you tell your new story. We’ve been supporting the energy industry around the world for nearly 30 years. We’re passionate about it. We talk your language and we impress with our work each and every day. Our understanding of your problems is one of our differentiators. Another is our results-based approach, using our skills to generate quality sales leads for you.

If you have plans to transform your business let us know how we can help.